Free Loan Agreement Template

Use our Loan Agreement template to specify the terms and conditions of a loan.

-

1

Choose a form

Browse and select the document you need

-

2

Answer Questions

Go through our builder and complete your form in 5 minutes

-

3

Download & E-sign

Receive your document in PDF or Word format

Create Document

Create Document

- Download as PDF and Word

- Access from desktop, tablet & mobile

- E-signature

- Yearly Updates & Notifications

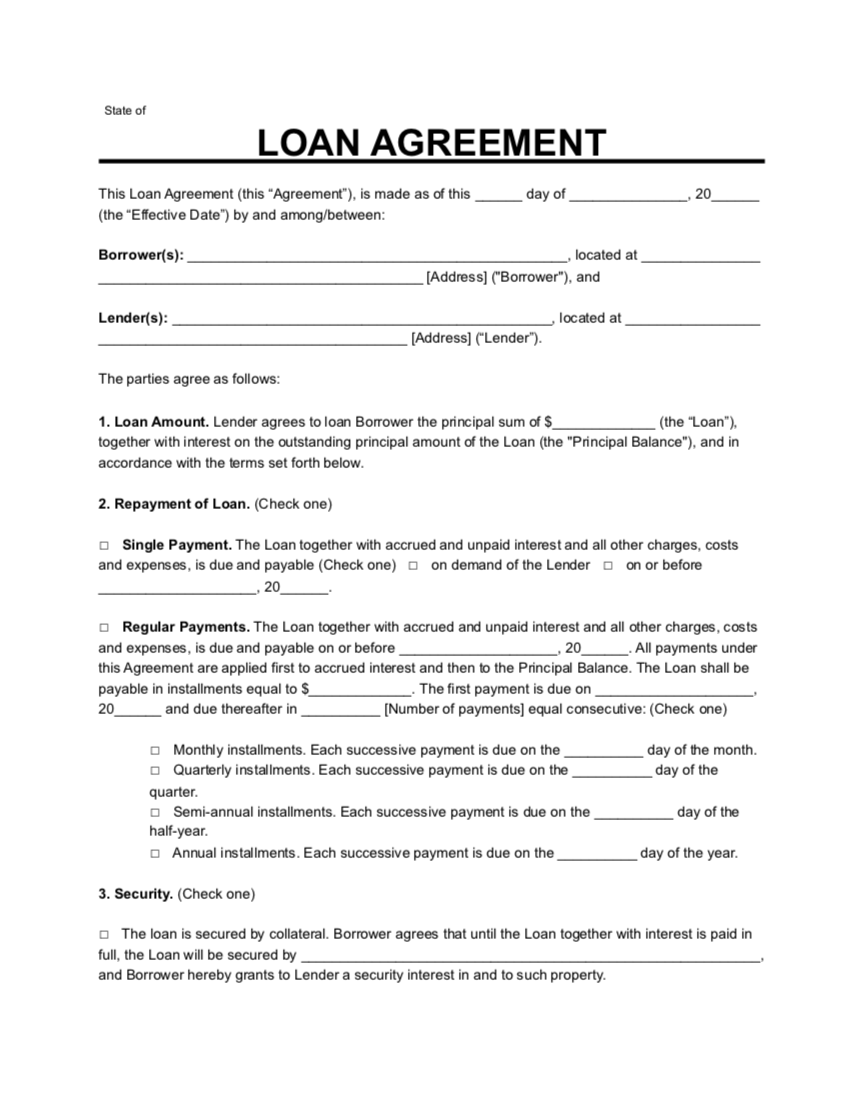

A loan agreement is a contract between a lender and a borrower that specifies the loan details, including the amount of money borrowed, repayment schedule, and interest rate, where applicable.

This type of legal contract is similar to a promissory note, but the latter is less formal and usually used when the loan amount is small.

Loan agreements are helpful whenever you lend or borrow money. This is a legally binding agreement that is enforceable if any party defaults.

What Is a Loan Agreement?

A loan agreement is a written contract between a lender and a borrower. The borrower agrees to repay the loan and any interest on a specified date through lump sum or monthly payments. A loan agreement often provides additional terms to govern the transaction and detail the loan process.

Why Do You Need a Loan Agreement?

There are many reasons to create a formal loan agreement, even if the transaction is between friends or family:

- A verbal loan contract may be unenforceable or challenging to prove.

- Parties can agree on the consequences of defaulting on the terms before any default occurs.

- It clearly outlines how the loan will be repaid, including any interest.

- A loan agreement details the terms parties agree, making it easier to enforce if a party defaults.

When Do You Use a Loan Agreement?

You can create a loan agreement for use in the following situations:

- Paying for tuition or other educational expenses with a student loan

- Personal loans between friends, colleagues, or family members

- Buying properties like cars, boats, furniture, or other significant expenses

- Starting a new business or investing more funds in a business

- Purchasing a home or other real estate properties

What to Include in a Loan Agreement

Your loan agreement form should contain the following key elements:

- Parties contact details

- Principal amount

- Interest (including interest payments, if any)

- Repayment details

If you’re unsure how to fill out these details, a loan agreement template can help you simplify the process, as you don’t have to create the document from scratch.

Frequently Asked Questions

Is a Personal Loan Agreement Legally Binding?

Yes, it is, as long as both parties sign the agreement.

Does a Loan Agreement Need to Be Notarized?

No, it doesn’t, although notarizing will help prove the document’s validity.

Does a Loan Agreement Need to Be Witnessed?

No, it doesn’t, although doing so may help to prove the parties’ identities.

How to Write a Loan Agreement

Follow these steps to write your loan agreement that will protect you if the borrower fails to pay you back or defaults on the loan.

1. Write the Name of the Parties

Always ensure you write the parties’ legal names. If one party is a business entity, use their registered name as it appears on their incorporation document.

2. Write the Loan Amount

State the principal amount you’ll be lending to the borrower.

3. Outline the Repayment Schedule

Specify how the borrower will pay back the loan. It could be a lump sum on a particular date or made through instalment payments. You should also include a maturity date, which specifies when the loan payment must be fully reimbursed.

4. Specify the Interest Rate

State the loan’s interest rate as agreed by borrower and lender.

5. State Prepayment Options

Specify if the borrower can repay the entire loan early and if there will be any discount. Early repayment typically allows borrowers to reduce the interest owed.

6. Include Penalty for Default or Late Payment

State when the borrower will be in default and your rights in such situations. You can also add a guarantor, or a cosigner, to the agreement to protect yourself in case the borrower defaults on the payment.

7. Include the Resident Law

Decide the state law that will govern the transaction.

8. Specify How Parties Will Communicate

State your communication method.

9. State How You Will Resolve Disputes

There are several options: litigation, mediation, or arbitration.

10. Add Important Signatures

Include the signature of the parties to the transaction and that of any guarantors or co-signers.